Alphabet’s Waymo has recently announced its collaboration with Uber to bring self-driving vehicles to Austin and Atlanta. If this wasn’t clear from this news as well as the numerous other autonomous vehicle companies such as Zoox and Cruise, autonomy is not exclusive to Tesla.

Head of Research Raymond Tong trying a Waymo on a research trip

There are some differences between Waymo and Tesla worth highlighting. Tesla believes that a better trained AI model can achieve autonomy with cameras alone. This is a scalable strategy. Waymo on the other hand focuses on having a more advanced suite of sensors, including light detection and ranging (LIDAR) as well as making heavy use of location specific data. This is why it rolls out city by city.

There are some differences between Waymo and Tesla worth highlighting. Tesla believes that a better trained AI model can achieve autonomy with cameras alone. This is a scalable strategy. Waymo on the other hand focuses on having a more advanced suite of sensors, including light detection and ranging (LIDAR) as well as making heavy use of location specific data. This is why it rolls out city by city.

It is difficult to know whether focusing on safety or scalability would ultimately be the better approach for achieving overall success. However, what unites the two is their reliance on significant silicon content.

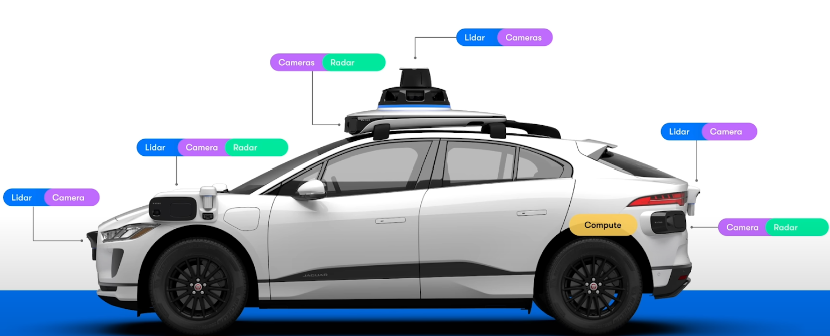

Making one vehicle autonomous in most situations

Both Tesla and Waymo make use of intricate onboard artificial intelligence (AI) modelling to predict other cars, pedestrians, road conditions and the like for safe driving. This is achieved by deploying a large number of sensors to build an image of the outside world. The vehicle then requires onboard compute hardware to interpret this image and react accordingly.

The sixth-generation Waymo has 13 cameras

Source: Alphabet

The onboard compute houses an AI model trained on clusters of datacentre accelerators. Tesla uses a combination of Nvidia GPUs and in-house Dojo chips, while Alphabet likely mixes Nvidia GPUs with its own Broadcom designed Tensor Processing Units (TPUs). The onboard hardware and the AI model (trained on data-centre hardware) combine to enable autonomy. That is to say, autonomy that can handle (hopefully) all possible variables on the road.

Autonomy is expensive

The trade-off for using so many sensors and training a robust AI model is cost. Tesla charges US$8,000 for activation of its Full Self Driving (FSD) service. Current Waymo rides are more expensive than their human controlled Uber counterparts – the upfront costs of the hardware more than offsets the cost savings of removing the driver at this stage. Not to mention they come with higher wait times and are geographically limited to a handful of U.S. cities.

Semiconductors advance over time as die nodes shrink and architecture is refined. Sensors, onboard computers and the AI models (underpinned by datacentre chips) will improve steadily, making this autonomy strategy more effective and/or cheaper over time. Once some of the newer componentry (like LIDAR) gets to scale, costs could fall more rapidly.

Meanwhile autonomy already exists in non-car vehicles

John Deere tractors and Komatsu mining equipment have been autonomous for several years. How have they succeeded where large automotive companies have not?

As in automotives, the autonomy Loftus Peak sees in heavy machinery is enabled by way of significant silicon input. John Deere tractors (pictured below) contain a myriad of sensors and an onboard computer like Nvidia’s Jetson Xavier IoT chip. However the silicon input for autonomy heavy machinery is much lower relative to cars. These tractors and mining trucks are not expected to operate in close proximity to other heavy machinery (unless that heavy machinery is also enabled with autonomy). This, and a lack of other variables, such as pedestrians, off-leash dogs and fire hydrants makes autonomy an achievable reality.

This modular Chisel Plow has sensors that communicate with the main tractor

Source: John Deere

The amount of sensors and silicon is increasing in all cars irrespective of autonomy.

Despite all the interest in electric vehicles (EVs) over the years, Loftus Peak believes the trend towards software defined vehicles is just as important when it comes to the disruption impacting the automotive market. The introduction of advanced driver-assistance systems (ADAS) features like lane keeping and obstacle warnings, as well as expanded onboard infotainment necessitate more silicon content. This trend is not limited to new EVs, but also ro their legacy internal combustion engine counterparts, currently a much larger market. This comes in the form of better connectivity, sensors, microcontrollers and centralised compute.

As far as investment by the portfolios that we manage, semiconductors are foundational to the roll out of these new features. Each new car needs more micro-controllers and ultrasonic sensors, such as those supplied by ON Semiconductor. Connectivity and logic chips are supplied by companies including Qualcomm, MediaTek, and Mobileye. Training AI models on the cloud for automotive autonomy utilises AI accelerators like those designed by Nvidia, Advanced Micro Devices and Broadcom. Meanwhile chips across these different functionalities must be fabricated. Often this is done by companies like Taiwan Semiconductor Manufacturing.

Offering new car features is an end unto itself. These features are being rolled out irrespective of whether or not it eventually leads to autonomy. This means the silicon content likely increases on a per vehicle basis, growing the top line of the semiconductor names listed above.

As the silicon volume increases on a per vehicle basis, cars will becomes more intelligent, predictable and interconnected. Even if they lack the higher end features like LIDAR or bespoke AI self-driving models, they may eventually put autonomy in reach of the automotive autonomy due to the pervasiveness of ADAS systems.

It’s hard to say how long it will be before all cars will drive themselves. The market seems to ascribe some of Tesla’s value to this future, despite the company still generating the vast majority of revenues from auto sales and very little from autonomy. Alphabet gets little credit because it’s a relatively small business relative to its parent, for now. Nevertheless, whichever way the world gets to automotive autonomy, we will need more semiconductors to do it – and in the meantime vehicles are getting smarter and more connected anyway.

In Loftus Peak’s view, the companies selling these semiconductors to automotive businesses appear to have little, if any, of this more connected and intelligent automotive future priced in and therefore make for attractive investment opportunities. Better yet, they are often well-diversified by selling to many other end markets. This provides valuation comfort when selecting semiconductor names to gain exposure to the disruption impacting the automotive industry.

Share this Post