By Alex Pollak – Chief investment officer – Loftus Peak

What next for Snapchat? After a disastrous earnings call, the stock fell 25% and came within 25c of breaching its issue price of US$17. Those that didn’t take the opportunity, brief though it was, to sell at US$24 might be feeling nervous. It is hovering around US$20 now, following the Trump slump.

For the record, and because it’s relevant to our process, we didn’t invest. But does a holding in Snapchat make sense?

The business is easy to like. With 170m monthly active users who on average spend around 30 minutes a day, the base is solid. The company is capitalised at US$23b – 40% more than Twitter, and 95% less than Facebook, with revenue of US$150m in the past quarter, up three-fold on the prior comparative, but down 10% on the December quarter. So there is growth – but probably not enough for a company with this valuation. We are not fanatical about the fact that monetisation opportunities are not yet fully evident, but the lack of some additional clarity on what they might be is one of the reasons we didn’t invest.

Going into the float, Snapchat marketed itself not as Facebook (an advertising company) but as a “camera” company. This is very interesting – first because its revenue selling cameras is tiny (from Snapchat spectacles) and second because companies selling hardware tend to trade at very significant discounts to those selling software and systems. If Apple were to trade on a Facebook or even Google multiple, the stock price would more than double.

But Snapchat is getting advertising revenue – in the past few months, Spotify and Netflix have started advertising on it (The Netflix ad is above). Advertisers can also pay to use a photo filter, for example superimposing the account holder’s face onto a Batman picture, to promote the Batman movie. This appeals to young users, obviously.

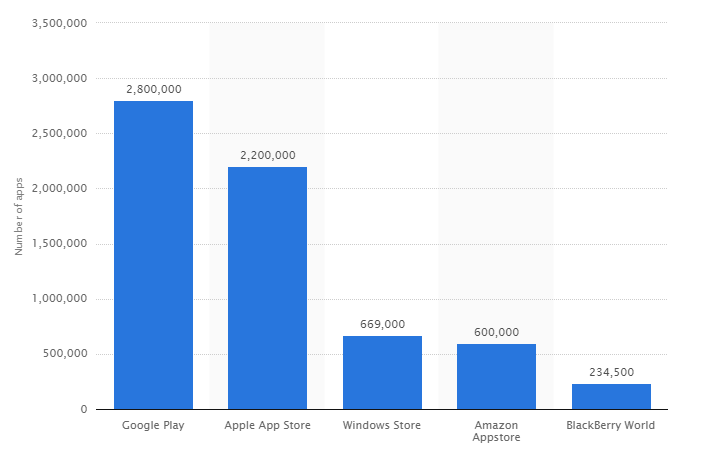

But Snapchat has made some very significant mistakes in its journey. One of the reasons for the success of Apple is the speed at which developers populated the App store with apps – 350,000 in the three years after launch in 2008. This is correctly recorded as one of the major drivers of success for the phone. And it was also the reason that virtually all other non-Apple phone makers were forced to adopt Google’s Android operating system; they could never get the number or variety of applications from developers as stand-alone companies (The Samsung app store exists, but it’s really an Android app store. Microsoft Windows also has an App store, but its relative size is a significant impediment to phone purchasers). It was only recently that Android surpassed Apple as the number one app store (2.8m v 2.2m for Apple, though Apple does contest this). Of course, good app developers get paid for their efforts, either by users through subscription, or through advertising.

Number of Apps in App Stores – March 2017 Source: Statista

But Snapchat, to its apparent detriment, has declined to play nice with developers, arguing that it isn’t ready to have its core product monetised by third parties. In so doing, it also hopes to keep more revenue for itself.

Whatever. But it has resulted in this questionable amount of revenue growth, which is why the stock fell.

And then there is Facebook. With ten times the number of users across three core products (Facebook, Instagram and Whatsapp) the company has a ‘take no prisoners’ approach to Snapchat, shamelessly copying features at will: Snapchat has Stories, Instagram launched stories. Snapchat has facial filters, Instagram followed. And so on.

On the conference call, Snapchat founder Evan Spiegel somewhat capriciously observed “just because Yahoo has a search box doesn’t mean they’re Google.” It didn’t go down well and was frankly an inappropriate comparison – Yahoo has executed very poorly against Google across a series of categories, including search, and that cannot be said about Facebook, which has delivered in spades in its own right and as a Snapchat competitor.

Fans of Snapchat believe think Spiegel is right on the Yahoo/Google thing, claiming that Snapchat is much more personal and intimate, and is often the medium of choice when truth is to be told. Maybe, but it may not be enough.

What has also not escaped the attention of investors is the critical role which Google is playing in the development of Snapchat. As noted in last week’s column on networks, in Snapchat’s IPO filing the company noted that its single largest cost was Google. It has committed to spend over US2b in the coming five years on that company’s services “some of which do not have an alternative in the market.”

Is that the sound of a big company exercising its power to extract a gatekeeper’s toll on a wannabe? Maybe. What is certain is Google and Facebook harvested two different but ultimately incredibly valuable datasets – the knowledge graph (Google) and the social network (Facebook) for free. It is unclear whether that could be done today from scratch. In China, the government virtually legislated out Google and Facebook, in favour of its homegrown versions Alibaba and Tencent and Baidu.

As a disruptor, Snapchat certainly makes the grade, monetising a demographic through a medium which upends many more traditional formats. It just isn’t the first to do so, and may therefore be in a weaker position. But it is the kind of stock we would review constantly, with a view to finding the right price.

Share this Post